- Tokenized U.S. Treasuries and gold remain the largest on-chain asset categories by value and adoption.

- Private credit platforms continue expanding as institutional lending activity moves on-chain gradually.

- Tokenized real estate remains small despite representing a massive traditional asset market.

RWA Tokenization continues gaining traction as treasury-backed and gold-backed assets dominate on-chain markets, while private credit expands steadily and real estate platforms remain in earlier development stages.

Treasury Assets Lead the On-Chain Market

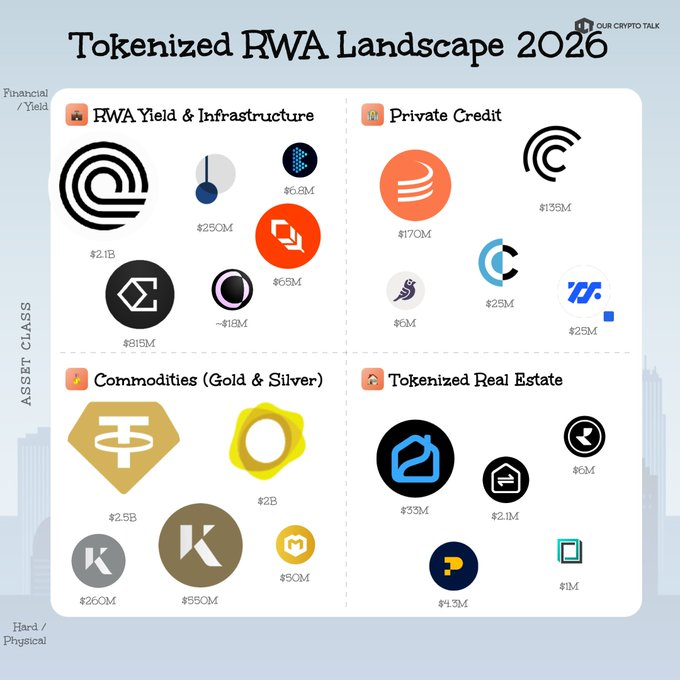

Recent industry data mapped leading tokenized asset categories. Treasury-backed products occupied the largest positions. Capital remained concentrated in yield-focused platforms.

A market update from ourcryptotalk shared the latest ecosystem breakdown. The report categorized projects by asset exposure. Treasury products accounted for substantial market value.

ONDO led the segment with approximately $2.1 billion exposure. ENA followed with roughly $815 million in assets. PENDLE recorded approximately $250 million in tokenized yield products.

The figures indicate sustained demand for income-generating assets. Investors continue seeking blockchain-based access to traditional yields. Consequently, treasury-backed products maintain strong market positions.

Gold Maintains a Strong Position Among RWAs

Tokenized commodities represented another major category within the landscape. Gold-backed products accounted for most commodity activity. Several projects accumulated significant market value.

XAUT led the commodity segment with approximately $2.5 billion. PAXG followed closely with nearly $2 billion. Additional projects expanded exposure across gold and silver markets.

The category also included KAU and KAG. Their asset values reached approximately $550 million and $260 million. XAUM contributed another $50 million in tokenized gold exposure.

These products provide blockchain-based access to physical commodities. Settlement occurs through digital infrastructure rather than traditional channels. As a result, participation continues expanding across multiple regions.

Private Credit Expands While Real Estate Develops

Private credit emerged as a growing segment within tokenized markets. SYRUP recorded approximately $170 million in institutional loan exposure. CFG followed with roughly $135 million in structured credit assets.

Additional platforms included CPOOL, TRU, and GFI. Their focus ranged from borrower pools to emerging-market lending. Together, they demonstrated increasing diversification across tokenized credit products.

Real estate remained the smallest category in the report. PRO led the segment with approximately $33 million exposure. Other projects maintained considerably smaller asset totals.

RIO, PROPS, and BST collectively represented only several million dollars. Their scale remained modest compared with treasury and commodity platforms. Nevertheless, real estate tokenization continued building foundational infrastructure across the sector.

The broader landscape showed a clear capital distribution pattern. Treasury products and gold retained leadership positions throughout the market. Meanwhile, private credit expanded steadily while real estate remained an emerging segment.